Choosing Your Payment Processing Pricing

Choosing Your Payment Processing Pricing

At Best Side Payments, we believe in empowering you through comprehension. Our goal is to provide you with clear information, so you can make the best decision for your business.

We offer two transparent pricing models and will help you choose the option that fits your business best. Both models also allow us to donate a portion of the revenue generated from your account to a local nonprofit of your choosing.

Many large processors promote flat-rate pricing as a “simple” solution. In reality, these models bundle all costs together, and that simplicity often comes at a higher cost to the business. We believe transparency means helping you understand exactly what you are paying and why.

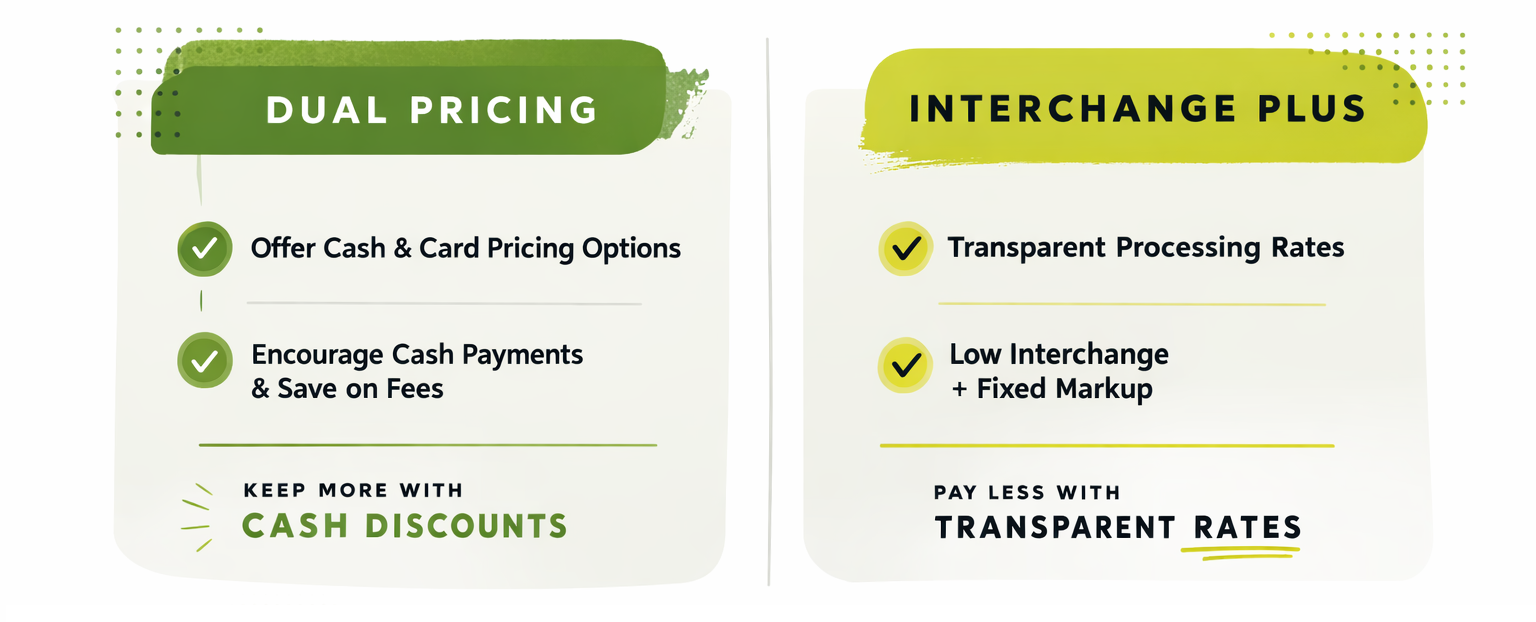

Dual Pricing

(also known as cash Discounting)

30% revenue goes to non profit of your choosing

Dual pricing allows businesses to offer two prices for the same product or service: a lower price for cash payments and a slightly higher price for card payments. The difference reflects the cost of card processing, allowing businesses to offset those fees while giving customers the choice of how they want to pay.

Dropdown for FAQs

-

At Best Side Payments, we believe business can be a force for good in the communities we serve. We personally support the causes and organizations that matter most to us. We have built our company around the idea that the work we do every day can also help strengthen the communities around us.

Our business model is designed to support both local businesses and local nonprofits. When merchants choose dual pricing, it allows our company to generate additional revenue, which increases our ability to give back. That means more support for the causes you care about and more resources flowing into the communities we all share.

Together, everyday transactions can create meaningful impact.

-

Customers using a card will pay an additional 3.5% of the total sales price before tax.

-

It is the most fair pricing model for your customers, as unintuitive as that may seem.

At Best Side Payments we are passionate about converting businesses to dual pricing. We are in alignment with consumer advocacy groups who promote what is best for those members of our community who are unbanked or underbanked.*

Each year, the credit card companies (VISA/MC/DISC/AMEX) raise the fees they charge to process credit cards. As these costs go up, it becomes one more expense businesses have to cover. Just like rent, supplies, or payroll, higher processing fees can eventually lead to higher prices for customers.

When the cost of products or services increases due to increasing cost of accepting credit card payment, the unbanked or underbanked customers effectively subsidize the credit card points and airline miles for those who have more banking freedom and opportunity.

Making the mindful choice to transition to dual pricing, you will no longer have to raise prices due to rising processing costs. This will ultimately protect those who are most vulnerable in the financial ecosystem.

*Unbanked or underbanked individuals do not have easy access to a regular bank account or credit cards. Some may not have a bank account at all, and others may have one but still rely on cash most of the time. Because they have fewer financial options and resources, they are often more affected by extra fees and costs than people who have full access to banking services.

-

Under the dual pricing model, businesses advertise the standard price of their goods or services with the cost of card processing already included. In compliance with Visa, Mastercard, American Express, and Discover guidelines, there is no requirement to disclose processing costs in signage.

Customers who choose to pay with cash simply receive a discount at checkout.

If you choose to adjust your pricing slightly when implementing dual pricing, some regular customers may notice, but small incremental price changes are a normal part of doing business and typically do not create significant customer pushback.

-

The simple answer is yes.

You may hear several terms for passing card processing costs to customers, including dual pricing, surcharging, and cash discounting. While each follows slightly different compliance rules, they all serve the same purpose: helping businesses offset the cost of accepting card payment.

Interchange Plus Pricing

(also known as cost plus)

10% revenue goes to non profit of your choosing

This is the most transparent and card-accurate pricing model.

Interchange - Fees set by the card networks (Visa, Mastercard, etc.). and paid directly to banks that issue credit cards. Every single card on the market has a different cost associated with it. There are literally thousands of individual interchange rates.

Plus - On top of the interchange fees set by the card networks, the processor adds a small, clearly defined markup. This markup is how the processor earns revenue and funds the services they provide, such as account management, customer support, risk monitoring, compliance oversight, reporting tools, and technology infrastructure

Example: Interchange + 1.00% (Cost+1.00%)

Dropdown for FAQs

-

At Best Side Payments, we believe business can be a force for good in the communities we serve. We personally support the causes and organizations that matter most to us. We have built our company around the idea that the work we do every day can also help strengthen the communities around us.

Interchange-plus pricing is designed to keep processing costs as low and transparent as possible, which means margins are smaller. Even so, Best Side Payments still donates 10% of the revenue generated from your account to a local nonprofit of your choosing.

Low-cost processing can still create positive ripples in our community.

-

We will save your business money.

The exact amount depends on your transaction mix. Interchange is not a single fixed rate. It varies based on factors such as card type, rewards levels, debit versus credit usage, in-person versus online transactions, ticket size, and industry category.

Before you sign any agreement, we will provide a complete pricing breakdown based on your most recent three months of transaction data. This includes an estimate of your expected processing costs and a clear comparison showing how much you could save each month and over the course of a year.

-

Flat-rate pricing can make statements simple to read because everything is bundled into one rate. The tradeoff is that bundled pricing often causes businesses to pay more than necessary. Interchange-plus pricing separates the true card costs from the processor’s margin, which creates more detailed statements but reflects the most accurate cost.

Our team helps you make sense of those details by reviewing your statements with you, explaining the different card types and fees, and showing you how your transaction mix affects your overall rate. The goal is to give you a clear understanding of what you are paying and why.

-

Interchange rates depend on several factors including card type, rewards levels, debit versus credit usage, whether the card is present, and your industry category.

-

Yes. While individual transactions vary, we can review your transaction history to estimate your effective rate and help you understand your overall processing costs.

-

Not necessarily. Our team reviews your statements with you and explains what the key items mean so you always understand where your money is going.